There is no single housing market in the UK. Conditions vary across the country, from regions to individual towns, and a tailored local strategy is key to successful sales and agency growth in 2026.

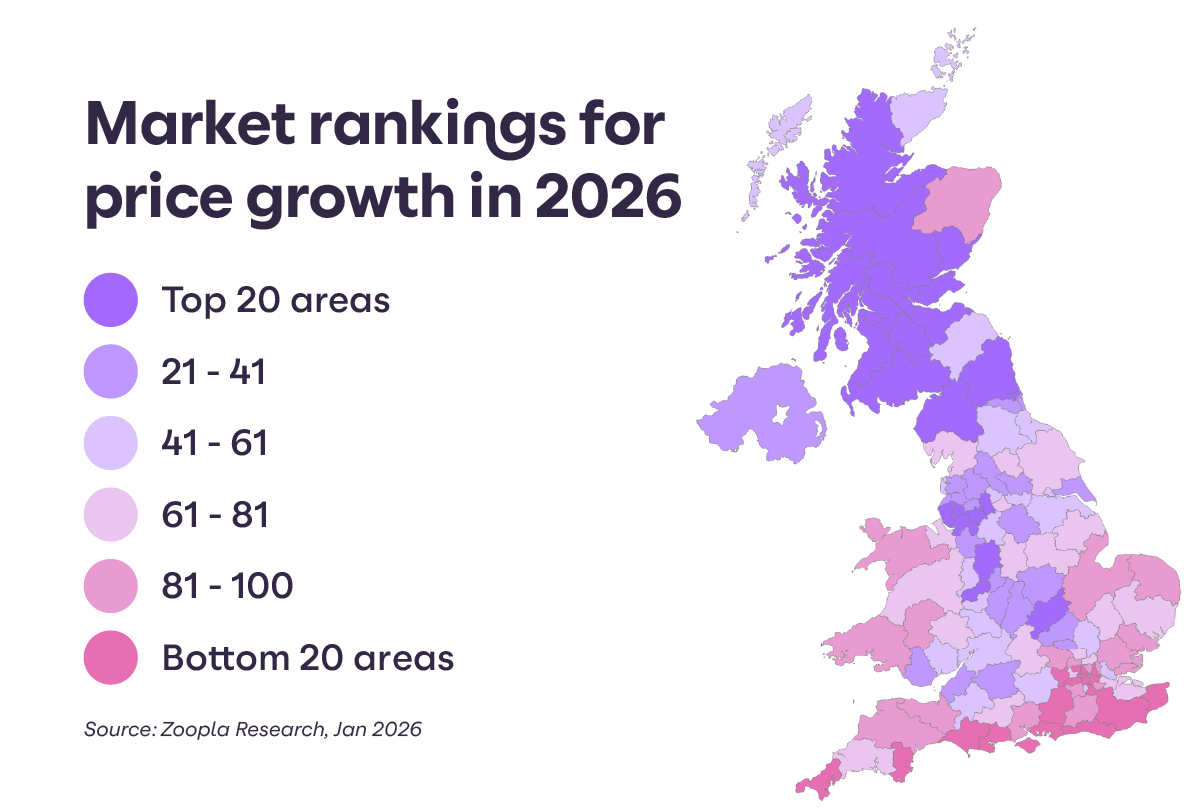

The Zoopla Sales Market Rankings 2026 use definitive data and key market indicators to predict the strength of the sales market across 120 postcode areas in the coming year.

The aim? Arm you with detailed local market insights to help inform client conversations, win more instructions and secure sales to support your growth in your local market.

The Zoopla Sales Market Rankings 2026

We predict that UK house prices are set to increase by 1.5% this year, but there will be a spread in the range of house price inflation across local markets. This will reflect the demand for and affordability of homes across the country, with markets in Scotland and Northern England enjoying the best prospects for growth.

In towns and cities at the top of the rankings, homes remain affordable or accessible to large employment centres, giving scope for more sales and price inflation. House prices across these areas are below the UK average and there remains a general scarcity of homes for sale.

Markets in Scotland lead the UK rankings, with just one of the top 10 coming outside the country. These markets have low levels of unsold stock meaning fewer asking price reductions and faster price growth.

Looking southward, the English market with the best prospects for 2026 is Wigan, closely followed by Liverpool and Stoke-on-Trent. Markets in the North West take up 6 out of 10 spots in the top 10, while markets beyond the North and Midlands don’t feature.

Housing markets across Southern England and London make up the list of the areas at the bottom of the rankings across the UK. This is largely down to affordability pressures resulting from higher house prices and the fact the market is still adjusting to higher mortgage rates. These markets have also seen a greater increase in homes for sale, boosting buyer choice, along with affordability impacted by higher stamp duty costs since April 2025. This explains the modest decline in average prices over the last year.

Kevin Shaw, National Sales Managing Director at Leaders Romans Group, shared his thoughts on the rankings:

“England is a patchwork of micro-markets. Every region has value pockets and premium pockets, and changing work patterns are widening where people feel they can live.

“In this report we can see ‘levelling up’ playing out and reflected in practical decisions (the political rhetoric having been forgotten). Better connectivity, stronger local economies and more flexible working post-Covid are widening options for buyers, renters and employers alike. In many cases, it makes the length and breadth of the country an option regardless of where employment HQs are located.

“In 2026, the winners won’t be regions - they’ll be the households that understand their local market and move decisively."