Win more instructions with Zoopla Masterclass

12 May 2026Get an edge with exclusive lessons from industry expert Ian Preston.

Read more

Rental inflation at 2.1% understates what most renters moving home are experiencing. Three-quarters of rental areas are growing faster than the national average. There are 25% fewer homes to rent than pre-pandemic levels which is keeping rent inflation positive.

The average UK rent is now £1,321 after growth of 2.1% in the last year

There are two distinct markets with rents rising 5% or more in affordable areas and at or below the UK average in pricier places

Average earnings are growing at twice the rate of rents, improving affordability for the third year in a row

London is the only region with rising rental demand (+6%) as higher mortgage rates keep renters in the market

Supply remains 20% to 30% below pre-pandemic levels in every region

We expect 2% to 3% rental inflation throughout 2026

Increasing rental supply is the best way to improve affordability

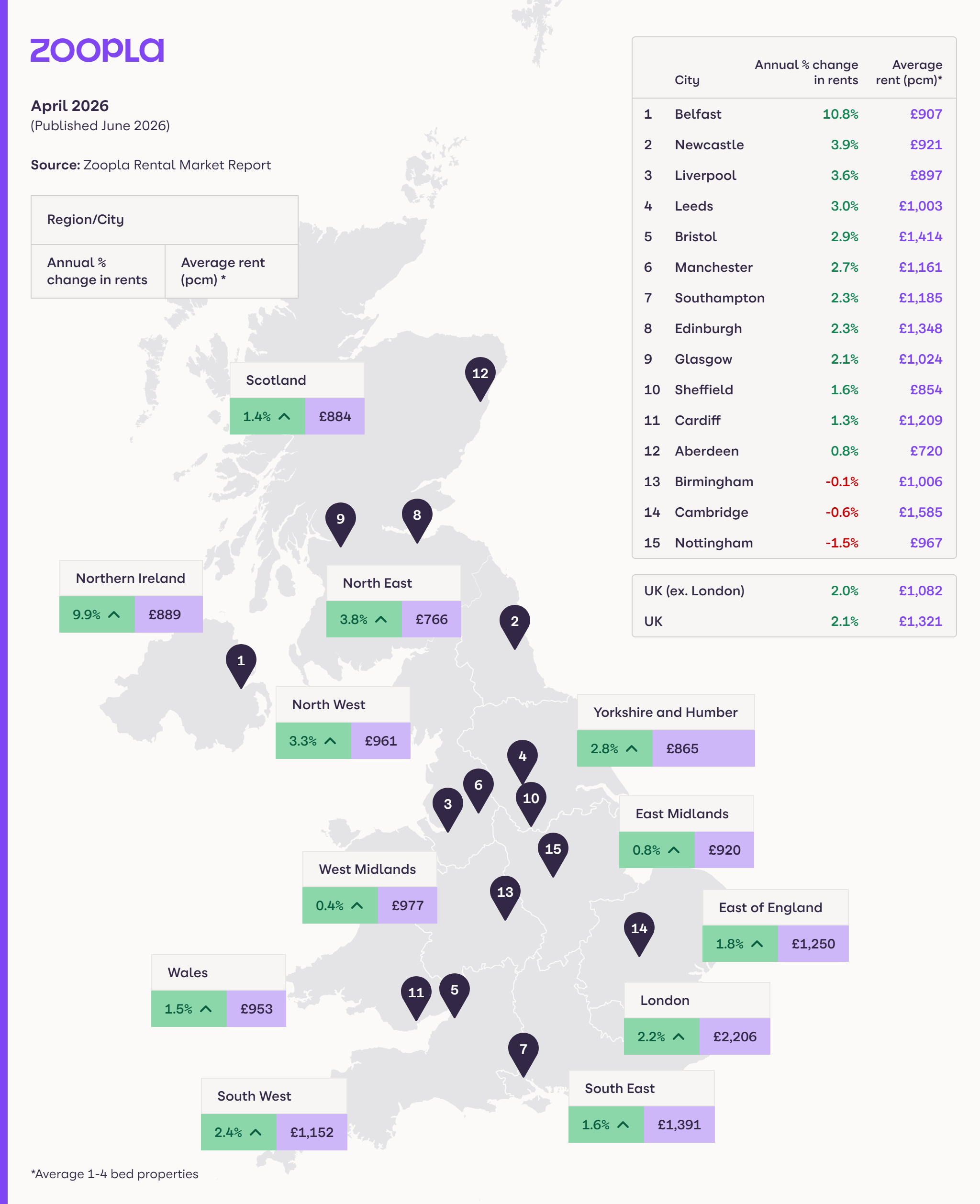

The average rent for new lets in the UK is £1,321 as of June 2026. This is a rise of 2.1% or £30 in the last year.

Average rent June 2026 | Annual rental growth (%) | Annual rental growth (£) | |

|---|---|---|---|

UK | £1,321 | 2.1% | £30 |

UK excluding London | £1,082 | 2.0% | £20 |

The 2.1% UK rental inflation rate doesn't reflect what most people are experiencing when moving. In reality, rents are rising faster than the national average in 75% of local areas.

This spike is being driven by shortage in available rental housing, with 25% fewer rental homes on the market now than before the pandemic. The lack of available properties is what keeps pushing prices upward.

Download the Zoopla UK Rental Market Report June 2026 (PDF, 345kB)

Better value, clearer results. Discover the new Zoopla packages, designed to help agents grow.

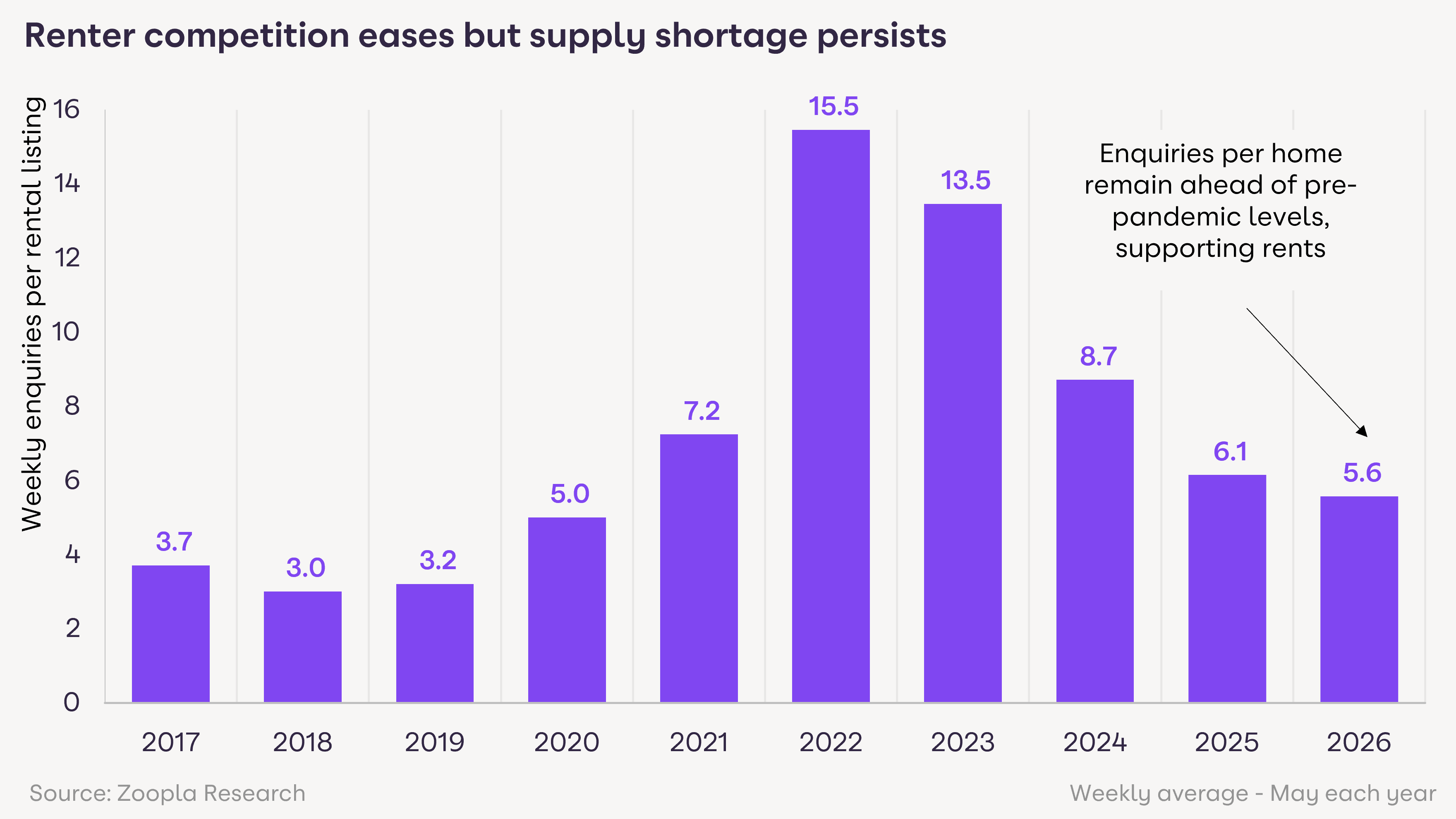

Average UK rents for new lets increased by 2.1% in April 2026, down from 2.6% a year ago. Competition for rented homes is falling, returning towards pre-pandemic levels.

There were an average of 5.6 enquiries per rental home in May 2026, down from a peak of 15.5 in 2022. But competition for homes remains well above 2017-19 levels and explains why rents are still largely rising.

Falling demand has not reduced rents because the number of homes available to rent remains below pre-pandemic levels across every region. New investment in private rented homes remains low.

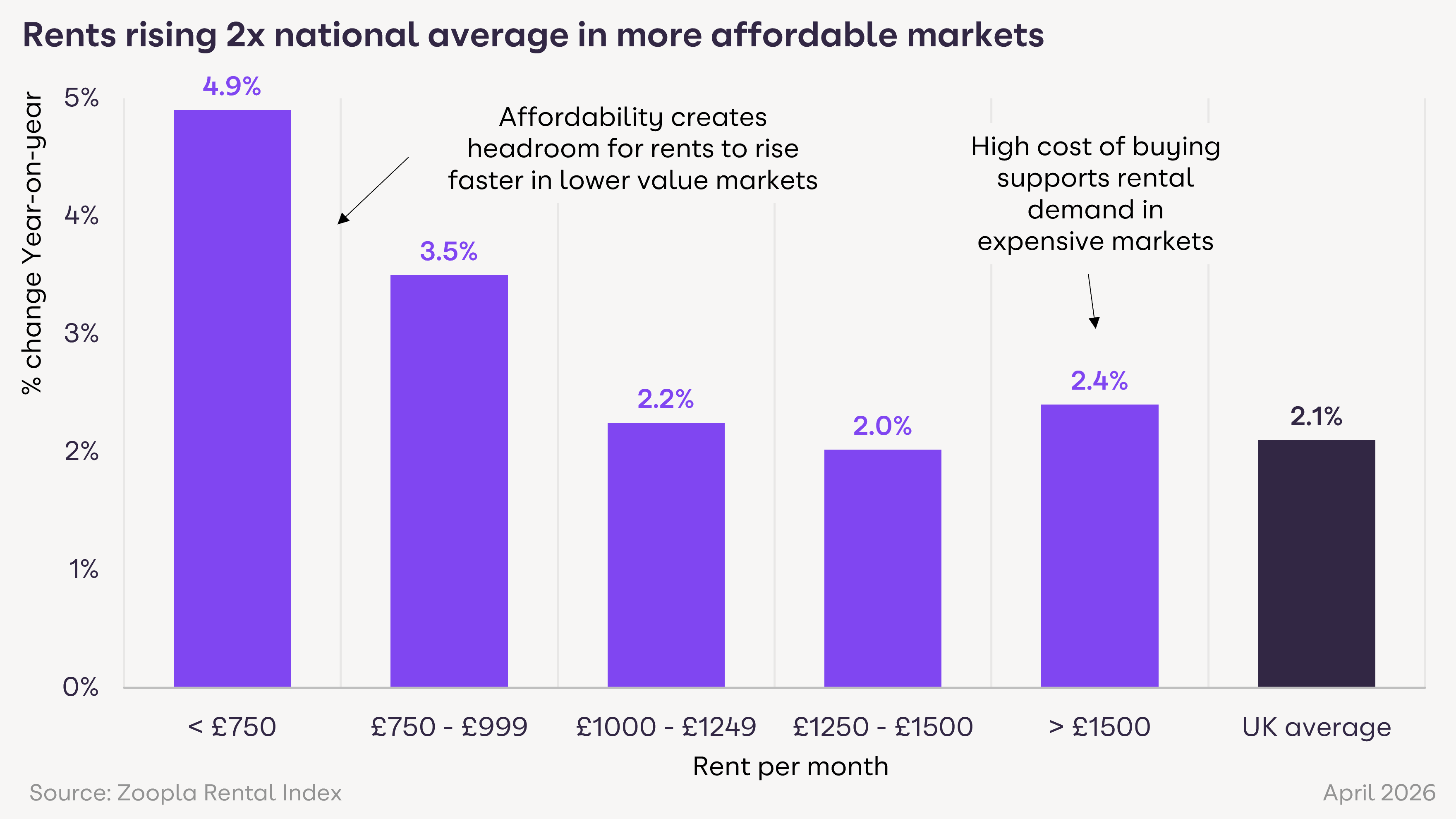

Behind the national figure of rental inflation are two distinct markets.

In places like Birmingham (-1.1%), Nottingham (-0.9%) and Bournemouth (-1.7%) rents are falling. Other areas like Carlisle (9.1%), Kilmarnock (9%) and Halifax (6.5%) are seeing rents rise at a rate of 7% to 9% per year.

Renters in areas with lower average rents are facing the fastest growth in rents. For example, rents in areas with an average of less than £750 a month are seeing nearly 5% year-on-year increases, more than double the national average

In more expensive areas, the high cost of renting is limiting how much rents can increase. Places with an average rent higher than £1,250 a month are growing at or below the 2.1% UK average.

The variation in rental growth is key for landlords and agents to understand in light of the Renters' Rights Act, which came into force in England on 1 May 2026.

The Act means that you can only increase rents once per year, it must legally be in line with market rates, and you must provide tenants with 2 months' advance notice of proposed increases. With rents rising at very different rates across the country, local market growth is an important factor in setting new rents and in how negotiations play out in practice.

Our data provides a factual basis for rent reviews between landlords and renters, highlighting the variance in direction and pace of rental growth in local areas.

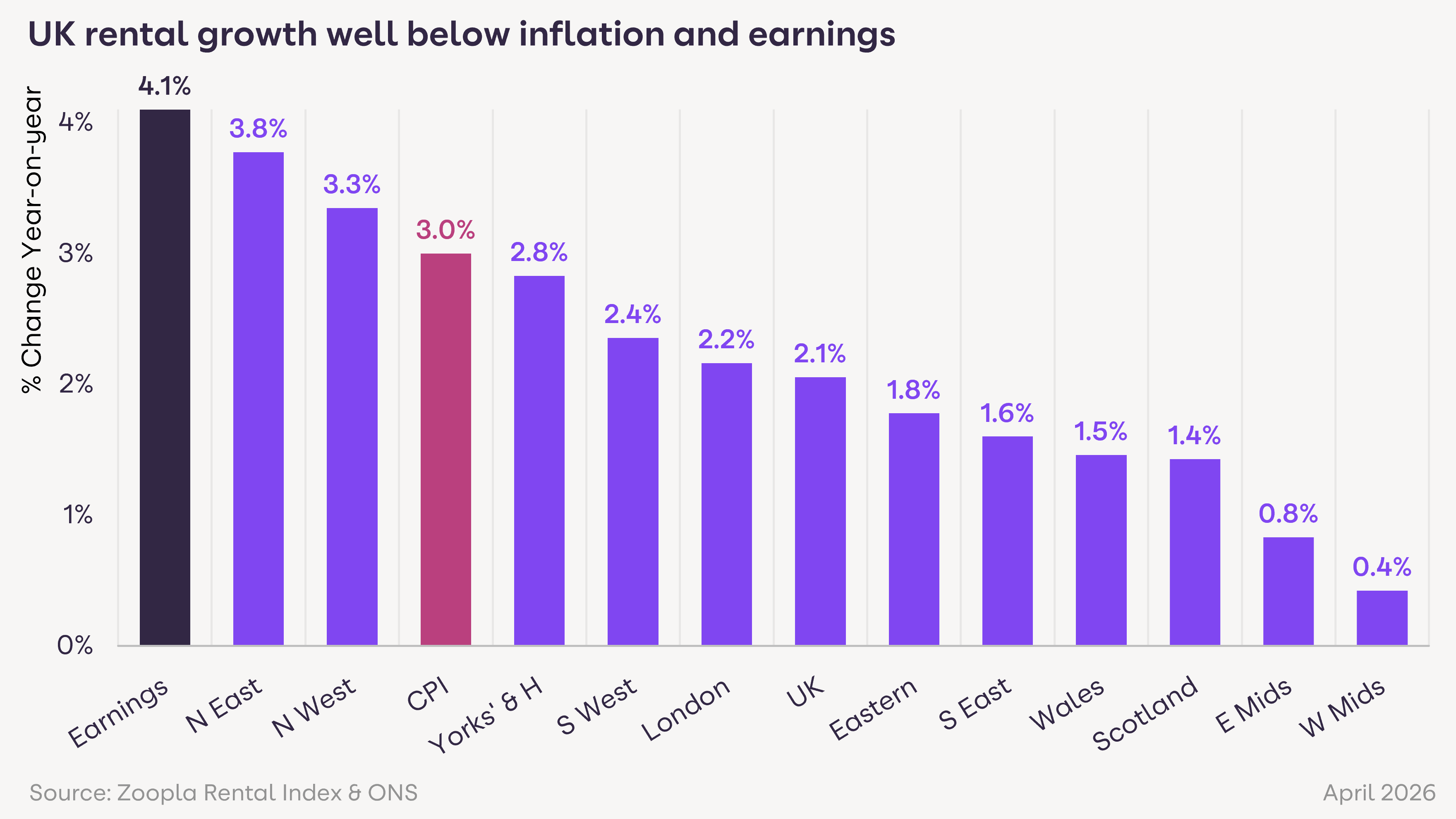

On a regional and countrywide basis, annual rental growth varies from just 0.4% in the West Midlands to 3.8% in the North East.

Average earnings are growing at 4%, almost twice as fast as the growth in rents. This offers some affordability relief for renters in full-time work.

The ease of buying a home has a direct impact on the rental market.

Higher mortgage rates have had the greatest impact on first-time buyers in London, where deposits and required income levels are highest.

This has led to an increase in demand for rented homes in London (+6% over the 4 weeks to 31 May 2026). It is the only region to register an increase in demand in this time.

With no change in the number of homes for rent, rental inflation in London has increased to 2.2%, up from 1.9% a year ago.

We expect rental inflation of 2% to 3% over the remainder of 2026. This would mark the third consecutive year in which earnings have outpaced rents, continuing a gradual improvement in affordability that began in 2024.

Rents will continue to increase at a faster pace in more affordable markets over 2026. Higher mortgage rates will continue to deter first-time buyers in more expensive cities, supporting rental demand and rents.

Growing the stock of homes for rent is the best long-term solution to improving rental affordability. Every region has fewer homes available to rent than before the pandemic and this structural shortage will keep rents rising faster than they otherwise would.

Our Rental Market Index is a repeat transaction index, based on asking rents and adjusted to reflect achieved rents. The index is designed to accurately track the change in rental pricing for UK housing.

The Zoopla Rental Market Report is first published on Zoopla.co.uk.

We try to make sure that the information here is accurate at the time of publishing. But the property market moves fast and some information may now be out of date. Zoopla accepts no responsibility or liability for any decisions you make based on the information provided.

Get an edge with exclusive lessons from industry expert Ian Preston.

Read more

UK house prices continue to show modest growth, up 1.4% year on year in June 2026, supported by easing mortgage rates and resilient demand in many regions. Market activity varies across the UK, with improving affordability helping to stabilise conditions.

Read more

With unrealistic pricing by sellers the key reason homes are unlikely to sell, our latest research explores how agents might help reset their expectations and win instructions rooted in achievable pricing.

Read more